Fascination About Hsmb Advisory Llc

Table of ContentsSome Known Incorrect Statements About Hsmb Advisory Llc Getting My Hsmb Advisory Llc To WorkGetting The Hsmb Advisory Llc To WorkExcitement About Hsmb Advisory LlcHsmb Advisory Llc - TruthsNot known Details About Hsmb Advisory Llc Unknown Facts About Hsmb Advisory Llc

In either case you need to obtain a certification of insurance coverage explaining the stipulations of the team plan and any insurance fee. Generally the maximum amount of coverage is $220,000 for a home loan and $55,000 for all various other financial debts - https://www.cybo.com/US-biz/hsmb-advisory-llc. Credit rating life insurance policy need not be bought from the company giving the car loan

The Facts About Hsmb Advisory Llc Uncovered

Nonetheless, home collections are not made and premiums are sent by mail by you to the agent or to the business. There are certain variables that have a tendency to raise the expenses of debit insurance even more than normal life insurance coverage plans: Specific expenditures coincide regardless of what the size of the plan, so that smaller plans issued as debit insurance coverage will have higher costs per $1,000 of insurance than larger dimension normal insurance coverage plans.

Since early gaps are pricey to a company, the expenses should be passed on to all debit insurance policy holders. Considering that debit insurance coverage is designed to consist of home collections, higher compensations and charges are paid on debit insurance policy than on regular insurance coverage. In a lot of cases these higher costs are handed down to the insurance holder.

What Does Hsmb Advisory Llc Do?

Where a business has different premiums for debit and regular insurance it may be feasible for you to acquire a bigger quantity of normal insurance policy than debit at no added price. Therefore, if you are thinking about debit insurance, you need to definitely examine routine life insurance policy as a cost-saving option.

Some Known Details About Hsmb Advisory Llc

Joint Life and Survivor Insurance provides insurance coverage for 2 or more persons with the survivor benefit payable at the death of the last of the insureds. Costs are dramatically reduced under joint life and survivor insurance coverage than for policies that guarantee just one individual, given that the likelihood of having to pay a fatality insurance claim is lower.

Costs are considerably more than for plans that insure one individual, considering that the possibility of needing to pay a death claim is greater. Endowment insurance attends to the repayment of the face total up to your recipient if death happens within a specific time period such as twenty years, or, if at the end go to website of the particular duration you are still alive, for the settlement of the face amount to you.

Adolescent insurance supplies a minimum of protection and might give coverage, which may not be readily available at a later date. Amounts supplied under such coverage are typically restricted based upon the age of the child. The present constraints for minors under the age of 14 (https://us.enrollbusiness.com/BusinessProfile/6637278/HSMB%20Advisory%20LLC).5 would certainly be the better of $50,000 or 50% of the quantity of life insurance policy active upon the life of the applicant

Getting My Hsmb Advisory Llc To Work

Adolescent insurance coverage may be sold with a payor advantage cyclist, which supplies for waiving future premiums on the youngster's plan in the event of the death of the individual who pays the costs. Elderly life insurance policy, in some cases referred to as rated survivor benefit strategies, offers qualified older candidates with minimal entire life protection without a medical exam.

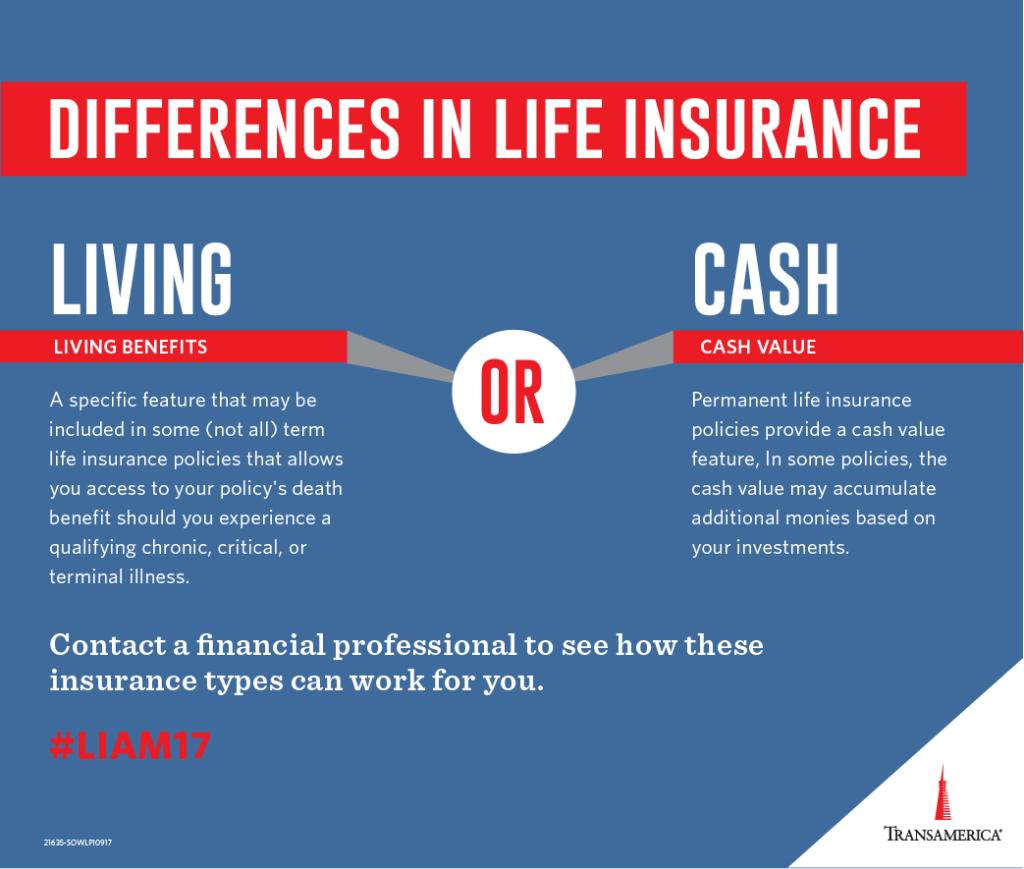

The objective of life insurance policy is pretty straightforward: in case of your death, life insurance policy will provide protection for your family and enjoyed ones to ensure their economic protection. Nevertheless, life insurance advantages differ by policy kind and each life insurance coverage strategy provides its very own set of benefits for the policy holder.

Versatile term sizes that can be customized based both on your family's requirements and budget plan. The advantages of High quality of Life Insurance policy include: Flexible and inexpensive term prices Quality of Life Insurance policies are not only economical considering that they cover several requirements, however they can likewise be changed to fit specific events in your life and allow you to access the cash benefit of your plan.

Some Known Factual Statements About Hsmb Advisory Llc

For even more info, go here. Coverage for clinical expenses and expenses. Whole Life Insurance Policy has no protection expiration day it lasts your entire life. You simply get the policy insurance coverage and maintain paying the same costs rate throughout your working and retirement years. The advantages of Whole Life Insurance coverage include: Flexible coverage that can be transformed as your requirements transform.

There are likewise some unanticipated benefits of life insurance policy where your life insurance coverage plan can cover circumstances and objectives you could not have thought about.: If your companion is currently only responsible for your children, your life insurance policy might assist them pay for day care or an additional child care solution while they return to function.

The objective of life insurance is pretty simple: in case of your death, life insurance coverage will offer protection for your family members and liked ones to ensure their monetary safety. Life insurance benefits differ by plan type and each life insurance coverage plan offers its very own collection of advantages for the policy holder.

The smart Trick of Hsmb Advisory Llc That Nobody is Discussing

Versatile term sizes that can be customized based both on your family's requirements and spending plan. The advantages of Quality of Life Insurance include: Versatile and budget-friendly term prices Quality of Life Insurance coverage policies are not just affordable because they cover several requirements, however they can additionally be readjusted to suit certain events in your life and allow you to access the cash benefit of your policy.

You simply buy the plan insurance coverage and maintain paying the exact same premium rate throughout your working and retired life years. The benefits of Whole Life Insurance include: Flexible insurance coverage that can be altered as your requirements change.

There are also some unanticipated advantages of life insurance where your life insurance coverage policy can cover scenarios and objectives you may not have thought about.: If your partner is currently entirely responsible for your youngsters, your life insurance policy might help them pay for childcare or another child care service while they return to function. Life Insurance.

:max_bytes(150000):strip_icc()/Life-Insurance-a8aee8e3024145a8b454ea19df030418.png)